Brief Overview:

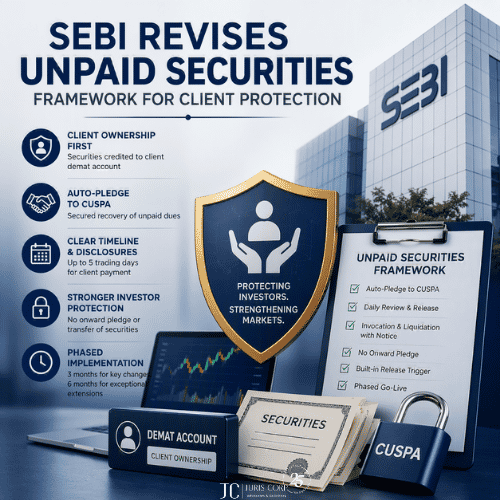

The Securities and Exchange Board of India (“SEBI”) has issued an amendment to the SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations dated May 05, 2025, effective immediately.

Technical Details:

A brief overview of amendments is provided below:

1) Scope of debt amended:

(a) Definition of debt has been amended to align it with the Reserve Bank of India (“RBI”) (Securitisation of Standard Assets) Directions, 2021 (“RBI SSA Directions”) include all financial assets permitted to be securitised which are originated by RBI regulated entities.

(b) Securitisation of receivables arising from listed debt securities (excluding unlisted debt instruments) is now permitted.

(c) The scope of permitted securitisation includes:

(i) equipment leasing receivables;

(ii) rental receivables; and

(iii) Trade receivables (arising from bills or invoices duly accepted by the obligors).

2) Securitised Debt Instruments (“SDIs”) to have a minimum ticket size of INR 1 Crore only for RBI regulated entities at initial subscription, and for non-RBI regulated entities at both initial subscription and subsequent transfers. Minimum ticket size for SDIs backed by listed securities shall be the highest face value among such underlying listed securities.

3) Minimum Retention Requirements (“MRR”) is aligned with the RBI SSA Directions, MRR to be 5% in case of receivables of tenor up to 24 months and 10% in all other cases.

4) Minimum Holding Period (“MHP”) is aligned with the RBI SSA Directions for debt by regulated entities. SEBI to prescribe the MHP norms for other kind of debt by non-regulated entities.

5) No single obligor will constitute more than 25% of asset pool being securitized. However, SEBI reserves the discretion to provide relaxations.

6) Originators and Obligors to have a track record of three financial years of operation in the type of receivable / debt they intend to securitize (not applicable for securitisation of debt by regulated entities).

7) More than 50 investors in an SDI issuance will be deemed to be a public issuance.

8) Clean up call to be optionally available to the originator at a maximum of 10% of the original value of the underlying (in lines with the RBI SSA Directions), such that they do not serve as a mechanism to provide credit enhancement.

9) Issue of SDIs shall be open for a minimum of 2 working days and not more than 10 working days.

10) Trustees’ for SDIs to be covered by the SEBI’s debenture trustee regulations.

11) SDIs to be fully paid up and in demat form only.

JC Takeaway:

The amendments to the SEBI SDI Regulations introduce key changes to the securitisation framework, impacting issuance requirements, investor eligibility, and operational guidelines, thereby shaping the regulatory landscape for listed securitisation market in India. These amendments are largely in line with the consultation paper proposals.

For further details, please see:

SEBI | SDI Regulations Amendment

For any queries/clarifications, please feel free to ping us and we will be happy to chat: