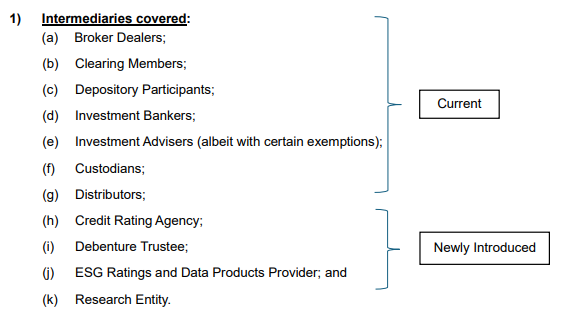

Currently the regulatory framework for Capital Market Intermediaries (CMI) in the International Financial Services Centres (IFSC) is laid down under the under the IFSCA (Capital Market Intermediaries) Regulations, 2021 (CMI Regulations 2021).

In the recent past, several new activities have been permitted in the IFSC including the ecosystem for distributors, debenture trustees and global credit rating agency.

The International Financial Services Centres Authority (IFSCA) has proposed changes to the regulatory framework for CMI with respect to registration, regulation & supervision.

IFSCA has issued a consultation paper seeking comments from the stakeholders on the proposed CMI regulations.

2) Proposals:

(a) Research Entities – new category

Research on securities and market products is a regulated activity in several jurisdictions including mainland India where the Securities and Exchange Board of India (SEBI) oversees it. IFSCA has now bought such entities under the scope of CMI. This means that entities providing research reports on securities or financial products including issuing ‘buy/sell/hold’ recommendations, setting price targets etc. will now be regulated under the proposed CMI framework.

(b) Guidelines applicable to distributors and ESG Ratings & Data Products Provider subsumed

Distribution and ESG Rating & Data Products Provider as an activity are governed by specific set of guidelines which establish a regulatory framework covering aspects such as registration, net worth requirements, fit and proper criteria, appointment of a principal officer and compliance officer, code of conduct, and continuous disclosure obligations. Under the revised framework, these guidelines have now been incorporated and subsumed under the proposed CMI framework.

(c) Allowing Broker Dealers to access Global markets

IFSCA currently allows authorized broker-dealers to access global markets. However, under the current regulatory framework, broker-dealer registration is only allowed through a recognized stock exchange. Therefore, a broker-dealer must first become a trading member of the exchange and subsequently obtain the exchange’s approval to access global markets.

Under the revised framework, broker dealers can access the global markets without the need to register itself as a trading member of a stock exchange in the IFSC. This provision is aimed at brokers who wish to access the global markets (either directly or on behalf of its clients) and allows them to register as a “broker dealer” directly with IFSCA without the need to become a trading member of a recognised stock exchange in the IFSC.

(d) Human Resources

There was a need for more clarity regarding the qualifications of the principal officers, compliance officers, and other key personnel of the IFSC unit. The revised framework now provides these clarifications. Sufficient manpower including the principal officer and the compliance officer are required to be based in IFSC. These requirements to apply to all the prospective appointments by a registered CMI after the date of notification of revised framework.

(e) Other Amendments

The revised framework also harmonizes the definitions with other notifications issued by the IFSC to ensure consistent applicability. Additionally, the net worth requirements for each CMI have been updated based on the representations made by the CMIs.

3) Takeaways

The primary aim of the new CMI regulations is to create a comprehensive framework for the registration, supervision, and regulation of various capital market intermediaries operating within the IFSC. These regulations also focus safeguarding the investors rights and protect the integrity of the market. Improving the ease of doing business for entities involved in the capital markets by simplifying and optimizing requirements is also a key feature. Furthermore, the new CMI regulations provide a regulatory framework for the introduction of new services in the capital markets within the IFSC.

The revamping of the CMI Regulations 2021 is also in line with the existing regulations, which require IFSCA to review the regulations every three years, considering global best practices, their relevance in the evolving market environment, and their alignment with the original objectives.

Comments on the consultation paper sought by 12th December 2024.