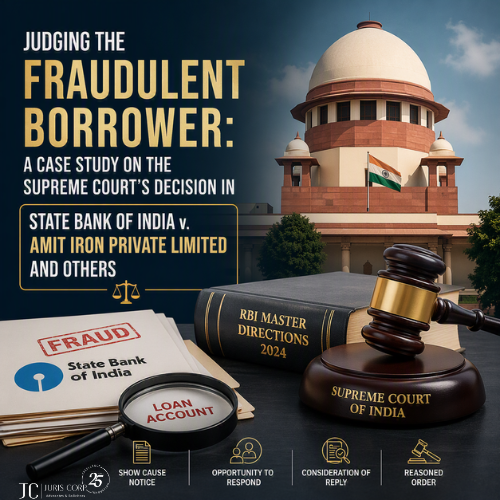

The banking regulator had laid down a clear and structured framework on classification of fraud – Reserve Bank of India (Frauds Classification and Reporting by Commercial Banks and Select FIs) Directions, 2016 (“Master Directions 2016”). The Master Directions 2016 were superseded by the Reserve Bank of India (Fraud Risk Management in Commercial Banks (including Regional Rural Banks) and All India Financial Institutions Directions, 2024 (“Master Directions 2024”). While the banking sector has been guided by these Master Directions over the years, it has also been entangled in litigation from borrowers when it comes to compliance with the procedural requirements and adherence to principles of natural justice under these Master Directions, and the manner in which they are implemented. Both Master Directions have been a matter of judicial scrutiny and the Supreme Court (“Court”) in State Bank of India v. Rajesh Agarwal[1] and State Bank of India v. Amit Iron Private Limited and Others[2] has carefully interpreted the Master Directions to reinstate its true spirit and eliminate any ambiguity surrounding procedural requirements.

Rajesh Agarwal: Master Directions 2016

In Rajesh Agarwal, the Court had the occasion to consider whether the principles of natural justice should be read into the Master Directions 2016, which were silent on granting an opportunity of hearing to the borrower prior to declaring the account as ‘fraud’. The Court held that the principles of natural justice (particularly the rule of audi alteram partem) have to be necessarily read into the Master Directions 2016 to save it from the vice of arbitrariness.

Regulatory clarification: Master Directions 2024

Following this judgment, the Master Directions 2024 were introduced which made a specific reference to Rajesh Agarwal in the context of serving a notice, giving an opportunity to submit a representation before classifying persons / entities as fraud and passing a reasoned order. In this context, the Master Directions 2024 incorporated Clause 2.1 (sub-clauses 2.1.1.1 to 2.1.1.4), to address the lacunae identified in Rajesh Agarwal.

Clause 2.1 of Chapter II of the Master Directions 2024 prescribes a mandatory four-step procedural framework, embedded within a board-approved fraud risk management policy, that must be followed before classifying an account as fraud. This essentially entails the following steps:

- Detailed show cause notice: Banks must issue a detailed show cause notice setting out the transactions, actions, and events forming the basis of the proposed fraud classification.

- Minimum response time: Borrowers and concerned persons must be given at least 21 (twenty-one) days to respond.

- Examining the response: Banks must maintain a structured system for considering replies and submissions before declaring an account fraudulent.

- Reasoned order: Banks must serve a reasoned order recording the relevant facts, the borrower’s submissions, and the reasons for classifying the account as fraud or otherwise.

While the Master Directions 2024 set out a lucid framework, it perhaps did not put a quietus to the issue entirely. The decision in Rajesh Agarwal read with its reference in the Master Directions 2024 was being interpreted to imply that it was mandatory for the banks to provide a personal hearing to the borrowers to make their representation prior to classifying the account as fraud, however providing the complete forensic audit reports to the borrower was not necessary. In view of this, the Master Directions 2024 came up for interpretation before the Court in Amit Iron.

Amit Iron: Issues and Facts

In the first appeal, State Bank of India had issued a show cause notice alleging irregularities indicative of fraud. After considering the borrower’s reply, the account was classified as fraud, and when challenged by the borrower, the Calcutta High Court held that a personal hearing and supply of the forensic audit report were necessary. In the second appeal, Bank of India had issued two show cause notices before classifying the account as fraud, which were set aside by the Delhi High Court for want of personal hearing. The following questions came up for consideration before the Court:

- Whether Rajesh Agarwal recognized an inherent right in the borrower to a personal or oral hearing before the account is classified as fraud?

- Whether the issuance of a show cause notice, consideration of the reply, and the obligation to pass a reasoned order would satisfy the principles of natural justice?

- Whether there was an obligation to furnish the entire forensic audit report, or whether furnishing the conclusions alone would suffice? The full report must be furnished, subject to narrow exceptions.

Reversing the momentum set in the aftermath of Rajesh Agarwal, the Court held that banks are not required to provide personal or oral hearings to the borrowers before classifying an account as fraud. However, banks must provide copies of audit reports (not merely the conclusion thereof), save and except portions relating to third-party rights. The judgment has further clarified that Rajesh Agarwal only contemplated notice, disclosure of forensic findings, and an opportunity to submit a written representation.

Understanding the rationale

The Court noted that the ultimate purpose of the Master Directions 2024 is to enable and ensure early detection and reporting of frauds, timely action against wrongdoers, and protection of banking stability. Delays in classification may prejudice recovery and investigation efforts by enabling dissipation of assets, destruction of evidence, or siphoning of funds. Fraud classification is therefore not merely punitive, but a preventive mechanism safeguarding public money and systemic integrity.

- Natural justice is flexible, not rigid

The finding to reject giving a mandatory personal hearing rests on the settled principle that the rules of natural justice are flexible and context dependent. Referring to the Constitution Bench decisions[3], the Court reaffirmed that a personal hearing is not an indispensable component of natural justice in every administrative proceeding and its denial would not by itself vitiate the process. The opportunity to submit a written reply to the show cause notice sufficiently satisfies the requirement of audi alteram partem. In this regard, the Court rightly relied on Chairman, Board of Mining Examination v. Ramjee[4] that natural justice cannot be expanded mechanically without regard to the practical realities of administration and the purpose of the regulatory framework.

- Banking and systemic considerations

The reasoning was not only driven by legal principles but also by the operational realities of the banking sector. Mandating oral hearings as a matter of right would fundamentally alter the nature of the process and frustrate the objectives underlying the regulatory framework. The Court noted the practical hurdles that could create roadblocks in achieving the objective of fraud classification altogether. A time bound process could become a prolonged adjudicatory exercise; multiple promoters or directors could insist on separate hearings; and delays could enable fraudsters to dissipate assets, destroy evidence, or abscond before investigation is initiated.

- Classification as ‘Fraud’ vs. ‘Wilful default’

The Court also rejected the argument that fraud classification proceedings must mirror the procedural safeguards available in case of classification as a wilful defaulter (which provides for a personal hearing before a review committee). Classification as fraud carries an element of criminality and the two are not at par.

- Need to provide forensic audit reports

The position held in Rajesh Agarwal that accounts cannot be classified as fraud without furnishing audit reports and granting a reasonable opportunity to respond, has been reaffirmed in Amit Iron. The reasoning is rooted in the principle that the material relied upon against a person must be disclosed to them[5] and the right to fair hearing includes the right to know the material forming the basis of the proposed action[6]. Furnishing the conclusions of the forensic audit report would not suffice, and the borrower cannot effectively respond to the show cause notice based on the conclusions.

- Limited exceptions to disclosure

The Court clarified that the right to disclosure is not absolute. Certain portions of the forensic audit report may be withheld by the banks where its disclosure would affect third-party interests. Even then, the bank would have to identify and communicate the basis of the proposed redaction to the borrower. The borrower must then be given an opportunity to explain why disclosure is necessary for an effective defence. Thereafter, the bank may decide to withhold the portions which impinge upon third-party rights.

Putting principles into practice: What banks must keep in mind

- Issue a detailed show cause notice setting out the transactions, actions, and events forming the basis of the proposed fraud classification. Banks should also take care that such notice is served through proper modes and at the correct address.

- Furnish copies of all relevant audit reports (including forensic audit reports) in a timely manner, and not just conclusions thereof. Exercising discretion to redact material is a narrow exception to be used sparingly and to avoid unnecessary delay.

- Grant time to submit a response as per the Master Directions 2024. However, granting an oral hearing is not mandatory.

- Banks are not required to permit cross-examination of forensic auditors or other persons, or legal representation as a matter of right during the process[7].

- Properly examine the borrower’s reply and submissions before arriving at any conclusion.

- Pass a reasoned order recording the facts, the borrower’s submissions; and the reasons for classifying the account as fraud or otherwise. A non-speaking order will remain vulnerable to challenge.

Conclusion

Although the Court has clarified procedural aspects in the process of classification set out under the Master Directions 2024, ensuring procedural fairness remains mandatory and centric. Even the exceptions carved out need to be exercised and applied by the banks carefully, and not in a routine manner.

The judgment serves as a guiding instrument for banks while implementing the process, and ultimately each classification as fraud would have to be assessed on a case-to-case basis. A one- size-fits-all approach cannot be applied. Even then, it cannot be ruled out that the defaulting borrowers may keep coming up with nuanced arguments to frustrate timely fraud detection and reporting, which is fundamentally a regulatory and administrative exercise intended to protect the banking system and public funds. It is therefore important for the banks to understand the reasoning embedded in the clarifications and then apply it to the facts of each case, rather than simply following a tick-box approach from a compliance standpoint.

Authors:

Saurabh Sharma

Partner,

Juris Corp

Email: saurabh.sharma@juriscorp.in

Aditi Sinha

Principal Associate,

Juris Corp

Email: aditi.sinha@juriscorp.in

Aakash Sinha

Associate,

Juris Corp

Email: aakash.sinha@juriscorp.in

[1] (2023) 6 SCC 1

[2] Civil Appeal Nos. 4243-4244 of 2026

[3] (1971) 1 SCC 396; (1971) 2 SCC 410

[4] (1977) 2 SCC 256

[5] (2022) 8 SCC 162

[6] (2023) 13 SCC 401

[7] (2019) 6 SCC 787