1. INTRODUCTION

Foreign Direct Investment

Foreign Direct Investment (“FDI”) refers to an investment made by a firm or individual in one country into business interests located in another country. Typically, FDI occurs when an investor establishes foreign business operations or acquires foreign business assets, including establishing ownership or controlling interest in a foreign company. It is distinguished from portfolio investments, where investors merely purchase equities of foreign companies.

One of the notable sectors influenced by FDI in India is the insurance sector. The Indian government, in the Budget 2025-2026, recently announced a significant policy shift, raising the FDI limit in the insurance sector from 74% to 100%. This article will delve into the implications of this change, comparing the old regulations with the revised norms, and analyze the potential impact on the industry and on the economy. This move is in alignment with many other countries such as Australia, Brazil, Canada and China, which allow 100% FDI in their insurance sectors.

IRDAI

The Insurance Regulatory and Development Authority of India (“IRDAI”) is an autonomous statutory body established by the Government of India under the Insurance Regulatory and Development Authority Act, 1999. Its primary role is to regulate and promote the insurance and reinsurance industries in India.

IRDAI is responsible for protecting the interests of policyholders, ensuring the financial soundness of insurance companies, and promoting fair, transparent, and orderly financial markets. It oversees both life and general insurance companies, ensuring they adhere to the regulations and provide efficient services.

Insurance for All by 2047

“Insurance for All by 2047” initiative is a strategic vision set by the Indian government and the IRDAI to ensure that every citizen has access to comprehensive insurance coverage by the centenary year of India’s independence. The initiative aims to address the current under-penetration of insurance in India and to achieve universal insurance coverage. The initiative aims, promoting financial inclusion by making insurance accessible to underserved and rural populations. It seeks to mitigate financial risks for individuals and businesses, thereby contributing to economic stability and growth.

2. CURRENT SCENARIO v/s THE REVISED NORMS

The Pre-2025 Scenario: Before the recent policy change, the FDI limit in the insurance sector was capped at 74% of the total equity share capital of Indian insurance companies. This limit was a result of progressive liberalization over the years, beginning with the Insurance Regulatory and Development Authority Act, 1999, which initially permitted FDI up to 26% of the total equity share capital of Indian insurance companies. Over the next two decades, this limit saw incremental increases, with the most significant one in 2021, raising it to 74% of the total equity share capital of Indian insurance companies.

Under the previous regulations, Indian insurance companies could attract foreign investment up to 74%, with the remaining stake held by domestic investors. This setup was designed to balance foreign capital influx and local control, ensuring that strategic decisions remained in Indian hands. However, while this limit allowed for substantial foreign participation, it also posed certain constraints:

- Limited Control: Foreign investors, despite having a significant stake, often had limited control over company operations and strategic decisions.

- Capital Constraints: The 74% cap meant that companies often faced capital constraints, limiting their ability to scale and innovate.

The Revised Norms: The latest policy change, raising the FDI limit to 100%, marks a transformative shift in India’s approach to foreign investment in the insurance sector. The key aspects of this new policy include:

- Complete Foreign Ownership: Foreign investors can now wholly own insurance companies in India without collaborating with Indian partners. This move is expected to attract more stable and long-term investments into the insurance sector.

- Enhanced Operational Control: With the ability to own 100% of the company, foreign investors will have greater control over operational and strategic decisions, enabling faster decision-making and implementation.

- Increased Capital Inflow: The removal of the FDI cap is likely to lead to a surge in foreign capital inflows, providing insurance companies with the financial flexibility to expand and innovate..

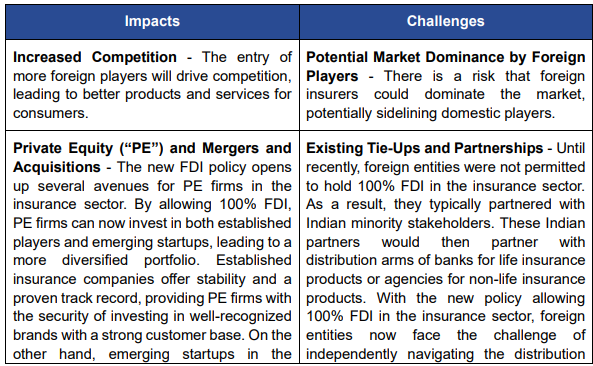

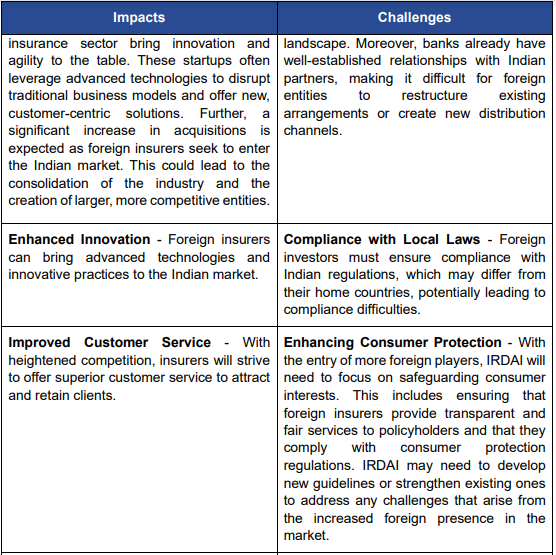

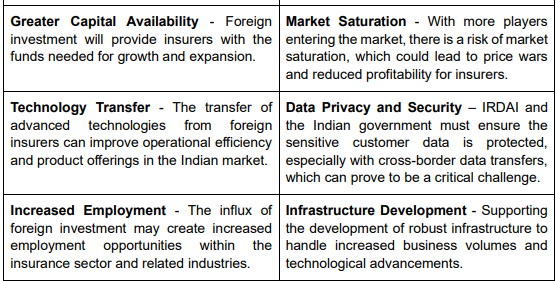

3, IMPACT AND CHALLENGES

The shift from a 74% to 100% FDI limit is anticipated to have profound implications for the insurance sector. However, it is not without its challenges:

4. CONCLUSION

The decision to raise the FDI limit in the insurance sector from 74% to 100% marks a significant milestone in India’s economic policy. While the increased foreign participation is expected to bring capital, innovation, and competition to the market, it also necessitates significant adjustments to IRDAI’s regulatory framework and strategic priorities. The authority will need to enhance its oversight capabilities, promote market stability, and ensure consumer protection to effectively manage the impact of this policy change. As IRDAI navigates this new regulatory environment, its ability to adapt and respond to emerging challenges will be crucial in ensuring the long-term success and sustainability of the Indian insurance sector.

As India continues to liberalize its FDI policies, the insurance sector stands at the cusp of transformative growth, poised to play a pivotal role in the country’s economic development. By comparing the older regulations with the revised norms, it is evident that the increased FDI limit is a step towards a more open and competitive insurance market, aligning with India’s vision of financial inclusion and economic prosperity.

The move is anticipated to influence the mergers and acquisitions landscape in the Indian insurance industry. Observers will need to see whether foreign investors opt to retain full control or seek partnerships with Indian counterparts. Such alliances could prove strategically beneficial in navigating regulatory frameworks, meeting consumer expectations, and managing dynamic distribution channels.

This step will also aid in unlocking the full potential of the Indian insurance sector, aligning with the vision of “Insurance for All by 2047”.