The need for more international resources to meet India’s net-zero target has made participation from international finance essential.

Given GIFT-IFSC’s role as a gateway connecting India to the global economy, a key challenge is creating an enabling framework for Transition Finance in a way that attracts international investors.

International Financial Services Centres Authority (“IFSCA”) has published a report[1] generated by Expert Committee on Climate Finance (“Committee”) for addressing climate change initiatives and the framework for decarbonisation in International Financial Services Centre (“IFSC”).

This report goes beyond defining Transition Finance to propose a comprehensive framework for mobilizing these investments through IFSC.

We will now delve upon the areas discussed in the report.

1. Strategy of the Committee Expanding Transition Finance Offerings at IFSC

- Scope and Definition:

- Define the boundaries of Transition Financefor clear investor guidance and risk management.

- Policy and Regulation:

- Develop a regulatory framework for the IFSC to govern Transition Finance activities.

- Recommend policies to the Indian government for efficient mobilization of Transition Finance through IFSC.

- Financial Instruments:

- Design new financial products for both assets and liabilities related to Transition Finance.

- Pilot these new products to build confidence among banks and financial institutions.

2. Concept of Transition Finance

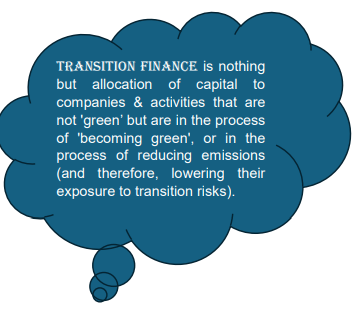

To understand the technical importance of Transition Finance and how it is achieving the hard end of decarbonisation it is important to differentiate it from ‘green finance’. Green finance entails securing funding for clean technologies which is a relatively straightforward proposition.

While Transition Finance aims to lower carbon emissions within hard-to-abate sectors which presents a far more complex challenge. These sectors lack a well-defined approach for financing, demanding a more nuanced and innovative strategy.

Green hydrogen, carbon capture, direct electrification represents the low-hanging fruit of emissions abatement in the industrial sectors.

3. Key Global Perspectives

The scope of Transition Finance defined by various authorities fluctuates between stringent to pragmatic approaches as mentioned below:

- EU Taxonomy: Defines transition activities as those lacking readily available clean alternatives, but demonstrably supporting a 1.5°C pathway and phasing out fossil fuels. Stringent criteria ensure reduced emissions and no lock-in of carbon-intensive assets.

- Japan: Emphasizes maximizing decarbonization efforts within existing sectors through efficiency measures until advanced technologies like carbon capture become viable.

- ICMA: A “transition” label signifies an issuer’s commitment to align business models with climate goals through strategic transformation.

- Asian Development Bank & G20: Define transition finance as supporting all sectors in transitioning towards net-zero emissions and climate resilience, aligning with the Paris Agreement and Sustainable Development Goals.

The Committee believes the EU’s approach may be too rigid for India’s current development stage. They favour broader definitions from Asian Development Bank and G20, reflecting economic realities.

4. Recommendations of Committee on Policy and Regulation

- Leveraging Existing Taxonomies Compliances

- Until the Indian Ministry of Finance establishes its own Green and Transition Finance Taxonomy, the Committee proposes to allow issuers to comply with recognized taxonomies from key global markets (as listed in the report). This caters to investors from diverse jurisdictions. For the purpose of implementing the same Committee has come up with the following recommendations:

- Assurance Mechanisms: IFSC should provide investor confidence through third-party assurance for compliance with chosen taxonomies.

- Clear Compliance Requirements: IFSC should clearly define compliance requirements for issuers, including:

- Adherence to at least one recognized taxonomy; and

- Filing compliance reports and third-party assurance reports with IFSC.

- Until the Indian Ministry of Finance establishes its own Green and Transition Finance Taxonomy, the Committee proposes to allow issuers to comply with recognized taxonomies from key global markets (as listed in the report). This caters to investors from diverse jurisdictions. For the purpose of implementing the same Committee has come up with the following recommendations:

- Tax Incentives:

- Offering tax benefits like a waiver or reduction of withholding tax for foreign investors in Transition Finance instruments issued through GIFT-IFSC can significantly reduce borrowing costs for companies until 2030.

- ECB Automatic Route

- The Committee further proposes to enable companies to raise funds for transition projects through the ECB automatic route, eliminating the need for lengthy approvals. However this process has a few obstacles:

- Limited End-Use Options: Restrictions to end-use prevent investments in crucial sectors like Smart Cities and water supply, hindering the potential impact of Transition Finance.

- Inflexible Maturity Requirements: The minimum 3-year maturity period discourages short-term investments needed for some transition projects, limiting the flexibility available to international investors compared to domestic options.

- Pricing Limitations: Current regulations cap the spread on ECBs, making longer-term investments (often preferred by lenders) less attractive due to restricted returns.

- The Committee further proposes to enable companies to raise funds for transition projects through the ECB automatic route, eliminating the need for lengthy approvals. However this process has a few obstacles:

- Enhanced ESG Disclosures by Companies:

- As a part of introducing a proper system for monitoring the projects the following compliances with regard to reporting are recommended:

- ESG disclosure for Corporates

- Expand SEBI’s Business Responsibility & Sustainability Reporting (BRSR) guidelines to include Net-zero targets and Decarbonization roadmaps.

- This transparency will encourage listed companies to embrace decarbonization, driving demand for Transition Finance to achieve their goals.

- Climate Risk Disclosures by Financial Institutions:

- Implement RBI’s draft paper on climate risk disclosures for banks. As banks set net-zero targets and aim to reduce financed emissions, they’ll require Transition Finance solutions for their corporate clients. This creates a significant demand for such instruments.

- ESG disclosure for Corporates

- As a part of introducing a proper system for monitoring the projects the following compliances with regard to reporting are recommended:

- Further Considerations:

- Similar disclosure requirements for insurance and pension regulators can further amplify demand and accelerate India’s decarbonization journey.

- Committee Recommendations on Financial Instruments

The following financial instruments have been recommended for allowing transactions in Transition Finance:

- Transition bonds/transition loans

- Convertible transition bonds/loans: Debt instruments with option to convert into equity at a predetermined level

- Equity/alternative investment fund: Equity/ Quasi Equity/ Convertible instrument

- Sustainability linked bonds/loans: Debt instruments with interest rate linked to predetermined outcome

- Sustainability linked derivatives: A derivative transaction with Key Performance Indicators (KPIs) built into contractual arrangements of SLD transactions.

- Carbon credits: Carbon credit is a tradable instrument used to monetize the value of carbon emissions. Two innovative examples of carbon credits involve Carbon Contract for Difference and an innovative Results Based Carbon Transition Bond.

5. Conclusion

The Committee has generated what can be considered a comprehensive blueprint that will guide sectoral regulators in India to stretch out detailed regulation in respective sectors to regulate Transition Finance. Given that global market is growing more and more efficient towards defining climate change regulations, enhancing the taxonomy and policies for transition finance can help implement a comprehensive framework thereby facilitating innovative structures in transition finance.