Brief Overview:

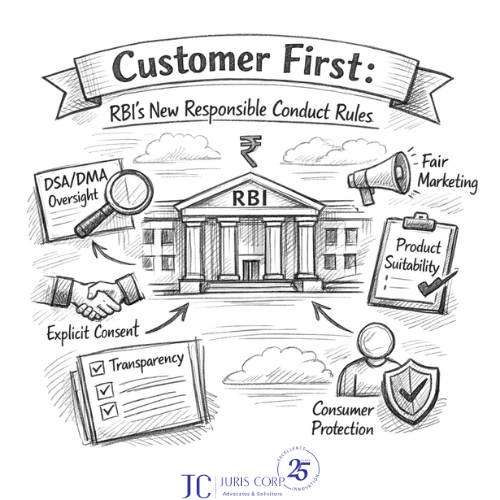

Comprehensive standards have been proposed for how banks and NBFCs advertise, market, and sell financial products, including third‑party offerings.

Comments on the draft directions can be submitted by 4th March 2026.

Technical Details:

Key Highlights

1) Marketing & Sales Policy

(a) Mandatory policy for selling own and third‑party products.

(b) Must cover suitability, feedback, and mis‑selling safeguards.

(c) If Direct Selling Agent (DSAs)/Direct Marketing Agent (DMAs) are used, eligibility, due diligence, training, audits, and non‑compliance actions must be defined.

2) DSA/DMA Governance

(a) Updated authorised DSA/DMA list must be published.

(b) Agents must be qualified and clearly identifiable.

(c) A binding code of conduct with penalties applies to staff and DSAs/DMAs.

3) Product Suitability

(a) Match product risks/features with customer profile, financial status, literacy, and risk tolerance.

(b) Suitability check is mandatory before any sale.

4) Conduct & Disclosure by DSAs/DMAs

(a) DSAs/DMAs must follow a comprehensive conduct framework.

(b) All disclosures to customers must be made before the sale.

5) Differentiation of Products

(a) Banks must clearly distinguish own products from third‑party products.

(b) Disclosures must be factual, transparent, and non‑misleading.

6) Definition of Third-party Financial Product or Service (TFPS)

TFPS includes any entity offering third‑party products/services to bank customers under agency or referral arrangements.

7) Permitted Scope – Insurance & TFPS

(a) Banks may act as insurance brokers departmentally.

(b) TFPS selling allowed only for regulated products under agency arrangements.

8) Agency Business Conditions

(a) Must be fee‑based only, with no risk participation.

(b) Clear disclosures required for all agency activities.

9) Explicit Customer Consent

(a) Separate explicit consent for each product/service.

(b) Consent only after terms & conditions are viewed.

(c) Easy opt‑out options must be provided.

10) Standard Definitions

Introduces definitions for bundling, mis‑selling, TFPS, DSA/DMA, explicit consent, and dark patterns.

11) Certification Requirements

All sales staff and DSAs must hold regulator‑prescribed certifications.

12) Separate Application Forms

Each product must have its own application form with clear features and risk details.

Takeaways:

The proposed amendments strengthen RBI’s framework to ensure fair, transparent, and customer‑centric sales practices by banks and NBFCs. Banks and NBFCs must also overhaul their sales governance through stronger DSA oversight, disclosure requirements, customer feedback mechanisms, and compensation norms.

For further details, please see:

Press Releases – Reserve Bank of India

For any queries/clarifications, please feel free to ping us and we will be happy to chat: