- Introduction

Japanese operating lease with call option (“JOLCO”) is a financing structure that enables airline companies the ability to expand their fleet and optimize capital efficiency. JOLCO combines the benefits of an operating lease with the flexibility of a purchase option at the end of the lease term. Under JOLCO, a Japanese special purpose company (“Japanese SPC”) which is typically backed by a combination of Japanese small and medium enterprise equity investors and financial institutions, purchases the aircraft and leases it to a lessee. While in principle, JOLCO is viewed as an operating lease as it provides the lessee with a genuine right to return the aircraft to the lessor at the end of the lease term, in practice, JOLCO often resembles financial leases. Unlike traditional Japanese operating lease arrangements, JOLCOs may be recorded in the lessee’s balance sheet as the lessee typically exercises the call option at the end of the lease term, effectively acquiring ownership after having enjoyed most of the benefits and risks associated with ownership during the lease period.

- Potential structure in the Indian context

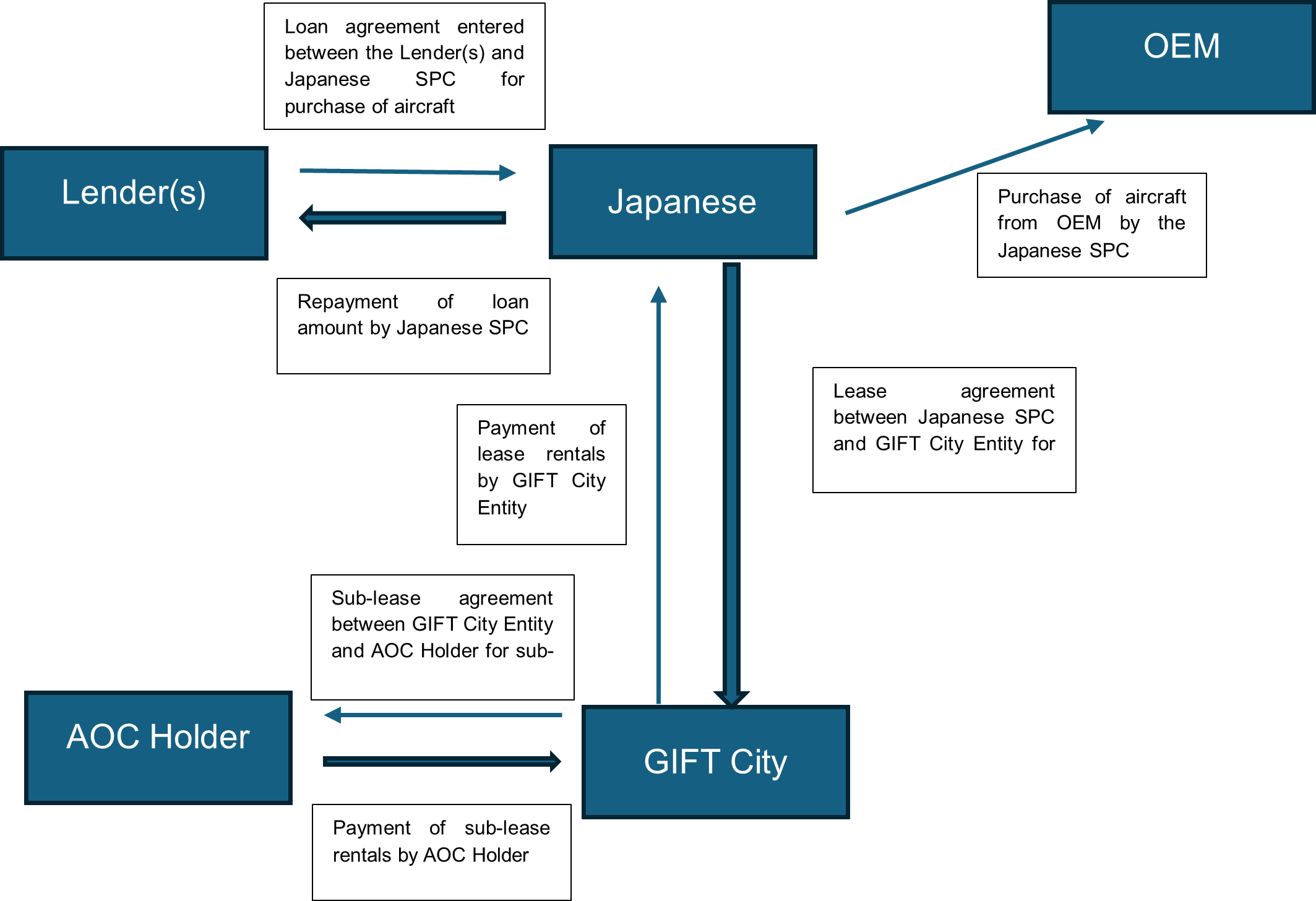

The Japanese SPC, as borrower, shall enter into a loan agreement with lending institution(s) (“Lender(s)”). Pursuant to the loan agreement, the Lender(s) shall provide the debt portion of the aircraft acquisition cost (usually consisting of 70-75% debt) to the Japanese SPC. The Japanese SPC shall utilize the debt portion and the equity portion (usually consisting of the balance 25-30% equity) invested by Japanese small and medium enterprise investors, to acquire the aircraft from an aircraft manufacturer (“OEM”). The Japanese SPC shall then lease the aircraft to an entity incorporated in the Gujarat International Finance Tec-City (“GIFT City Entity”), and the GIFT City Entity shall onward sub-lease the aircraft to the airline company in India (“AOC Holder”). The lease rentals payable by the AOC Holder to the Gift City Entity and by the Gift City Entity to the Japanese SPC shall be assigned to the Lender(s) and other finance parties. The aircraft itself shall be secured by way of mortgage.

- Key challenges in adopting JOLCO structures in India

Although there are instances of Indian airline companies using JOLCO structures (when in the mid-1990s, the then government owned Indian Airlines and Air India entered into JOLCOs with certain Japanese leveraged lessors as part of their fleet financing strategy for about 12 Airbus A320s), its adoption remains sparing in light of legal, regulatory, and structural hurdles. Some of these are as follows:

- Unfavorable tax withholding under the India-Japan double tax avoidance agreement (“DTAA”): Pursuant to the DTAA, lease payments are subject to a withholding tax of 10%, which has historically acted as a deterrent. Alternative leasing structures involving jurisdictions such as Ireland which has a more favorable tax treaty with India offers lower effective costs. However, with the option of leasing the aircraft to the Gift City Entity which in turn shall sub-lease the aircraft to the AOC Holder, the tax complications may now be mitigated.

- Complexity of multiple shareholder involvement: JOLCO transactions typically involve Japanese Tokumei Kumiai (“TK”) structures, which pool investments from multiple small and medium-sized investors. These shareholders often have voting rights and participate in key decisions, requiring their consent at various stages of the transaction. This adds a layer of governance complexity, especially in determining whether majority consent or unanimous approval is required, thereby often delaying processes.

- Classification as an operating lease: While JOLCO is economically akin to a financial lease, under applicable Indian foreign exchange laws, operating leases are not a recognized form of external commercial borrowing. Therefore, it is presently untested whether the Reserve Bank of India (“RBI”) would view such lease arrangements as operating leases or financial leases and whether prior approval of the RBI would be required for entering into such transactions.

- Structural incompatibility with current aviation lease models: Indian airline companies prefer setting up their own wholly owned subsidiaries in Gift City (“GIFT WOS”). The aircraft is typically leased to the GIFT WOS and then the GIFT WOS back-to-back leases the aircraft to the airline company in India. However, in a JOLCO structure, it is unclear whether the Japanese investors would be comfortable in leasing the aircraft to the GIFT WOS or would they rather set up their own GIFT City Entity. There are also complications surrounding the concept of beneficial ownership and foreign exchange challenges, which would need to be evaluated.

- Conclusion

While JOLCO structures offer a compelling and tax-efficient leasing solution internationally, its adoption in India remains largely untested due to regulatory uncertainties, structural mismatches and the operational complexity of involving multiple Japanese TK investors. However, the emergence of GIFT City as a growing international financial hub, along with the tax exemptions and regulatory flexibility available to entities established within it, presents a promising pathway for the potential adoption of JOLCO structures in India. As India continues to liberalize its leasing environment, particularly in the aviation sector, JOLCO may become a viable financing option for Indian airline companies in the times to come.

Authors:

Ankit Sinha

Partner, Juris CorpEmail:

Yashassvi PeriwalAssociate, Juris Corp

Vaishnavi PanyamTrainee, Juris CorpEmail:

vaishnavi.panyam@juriscorp.inDisclaimer:

This article is intended for informational purposes only and does not constitute a legal opinion or advice. Readers are requested to seek formal legal advice prior to acting upon any of the information provided herein. This article is not intended to address the circumstances of any particular individual or corporate body. There can be no assurance that the judicial / quasi-judicial authorities may not take a position contrary to the views mentioned herein.