All That Glitters: RBI’s Recalibration of Gold Metal Loans

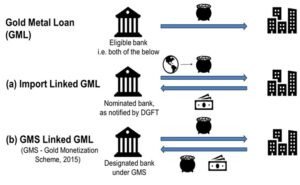

Gold has long served not only as a store of value but also as a financing tool within the banking system. In practice, gold‑based lending takes two distinct forms. Gold can be taken in form of a loan, and a loan can be taken against gold. To simplify, banks may lend physical gold to eligible borrowers such as jewellers and manufacturers, commonly referred to as Gold Metal Loans (“GML”) or they may extend loans against pledged gold, known as gold loans.

This article focuses on the evolving regulatory framework applicable to gold metal loans, with particular emphasis on recent developments.

A Gold Metal Loan may be provided in two principal forms, depending on the source of the gold. Under an import‑linked GML, nominated banks lend physical gold sourced from imports or other foreign sources to eligible borrowers. Alternatively, under a Gold Monetisation Scheme, 2015 (“GMS”) ‑linked GML, designated banks lend gold mobilised from public deposits, commonly referred to as localised gold.

Regulatory Framework

On June 6, 2025, the Reserve Bank of India (“RBI”) issued the Reserve Bank of India (Lending Against Gold and Silver Collateral) Directions, 2025 (“Old Regime”), laying down a comprehensive regulatory framework for lending against gold and silver collateral.

Subsequently, as part of its consolidation exercise, RBI, on November 28, 2025, issued the Reserve Bank of India (Commercial Banks – Credit Facilities) Directions, 2025 and the Reserve Bank of India (Small Finance Banks – Credit Facilities) Directions, 2025, which consolidated the Old Regime into the respective credit facilities frameworks; which were subsequently then amended (“New Regime”).

Set out below are certain key changes pursuant to the aforesaid consolidation.

Key Changes – The amendments as highlighted below shall come into force from 1st April 2026.

| Parameters | Old regime | New regime | Rationale |

| Eligible borrowers | The eligible borrowers include exporters of jewellery, domestic jewellery manufacturers who are not exporters of jewellery and the MMTC Limited for minting India Gold Coins. However, it was limited to gold jewellers who are themselves manufacturers of gold jewellery. | The ambit of eligible borrowers has increased to include jewellers who are not manufacturers themselves but outsource their manufacturing of jewellery on job basis to

any manufacturing firms / artisans / goldsmiths. |

It expands the pool of eligible borrowers, enabling banks to deploy additional capital across a broader borrower base.

|

| Tenor | For all the domestic jewellery manufacturers, who are not exporters of jewellery, the tenor of the GML shall not exceed 180 days. | For all GML other than lending to jewellery exporters tenor of the GML shall not exceed 270 days. | It provides level playing field across the class of borrowers. |

| Reporting requirement | There was no reporting requirement. | A supervisory return on GML must be reported to the RBI on a quarterly basis by seventh day of the following month. | The aim is to develop a supervisory management information system on GML. |

| Industrial use | It does not cover entities which use gold as a raw material, or as an input in their manufacturing or industrial processing activity. | No change. | While the submission was made by the market participant to include borrower which uses gold for other industrial use, RBI has clarified that the GML guidelines are primarily targeted at jewellery manufacturers and the demand from other sectors is not perceived to be significant. Additionally, RBI has further clarified that it has recently allowed need-based working capital finance to such non-jeweller borrowers, who use gold or silver as a raw material or as an input in their manufacturing or industrial processing activity. |

| Borrower differentiation | The framework does not prescribe any criteria for banks to determine whether a borrower qualifies as a manufacturer or a non‑manufacturer. This distinction is relevant given that gold imports are generally permitted only for manufacturers. | No change. | RBI stated that it is an operational matter, better left to the discretion of individual banks to frame their own policies. |

| End-use monitoring | There are no methodologies prescribed for the monitoring of end-use. | No change. | RBI stated that it is an operational matter, better left to the discretion of individual banks to frame their own policies. |

Factors for Consideration – The banks shall lay down a lending and risk management policy for GML including:

- Categories of GML which the bank desires to undertake;

- Limit on the quantity of gold that may be lent per borrower;

- Total quantity of the loans that may be outstanding at any point of time; and

- Detailed due-diligence requirements for deciding the eligibility of GML borrowers and their credit requirements.

Conclusion

The banks may decide interest rates based on costs of procuring and holding gold, and relevant spreads as per their interest rate policies. The recent amendments introduced by the RBI mark a positive step towards modernising the gold‑lending framework and strengthening a critical segment of India’s economy. By extending the permissible repayment tenor from 180 days to 270 days, the changes enhance operational flexibility and align GMLs more closely with borrowers’ working capital cycles. Further, the expansion of eligible borrowers to include non‑manufacturing jewellers who outsource manufacturing on a job‑work basis significantly broadens access to GMLs. Taken together with other revisions, these measures contribute to a more flexible, inclusive, and business‑friendly regulatory environment for Gold Metal Loans.

Authors:

| Saurabh Sharma Partner, Juris Corpsaurabh.sharma@juriscorp.in |

Dhwani Bansdawala Senior Associate, Juris Corpdhwani.bansdawala@juriscorp.in |

Kejal Soni Associate, Juris Corp Kejal.soni@juriscorp.in |

Disclaimer:

This article is intended for informational purposes only and does not constitute a legal opinion or advice. Readers are requested to seek formal legal advice prior to acting upon any of the information provided herein. This article is not intended to address the circumstances of any particular individual or corporate body. There can be no assurance that the judicial / quasi-judicial authorities may not take a position contrary to the views mentioned herein.